|

The

Liquidity Forecast Ladder is a model that

can

dynamically quantify the level of liquidity

over

an appropriate set of time horizons:

- in a

"business-as-usual" environment

- during a

liquidity crisis

The realization of the model in an MS Excel based

tool allows financial institutions to measure, manage and stress test

liquidity by projecting cash inflows and outflows arising from assets and

liabilities in dependence of input variables whose influence can be tested

under various scenarios.

Product features

The Liquidity Forecast Ladder consists of

two

core components:

|

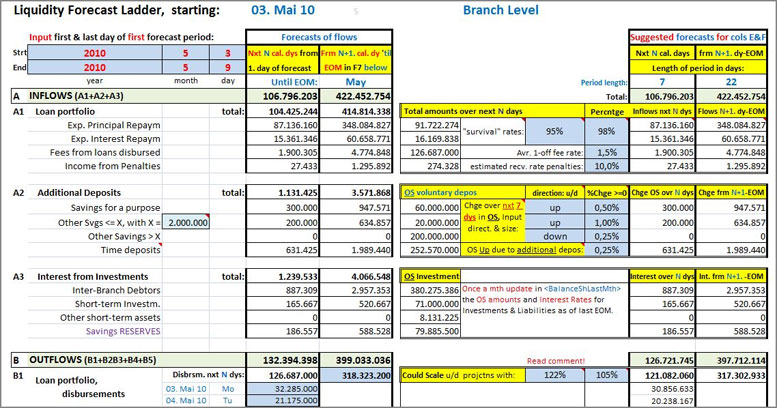

- The Branch Liquidity Forecast Ladder

covers two periods: the next N days (N <= 7) and from N+1st day

until end of month

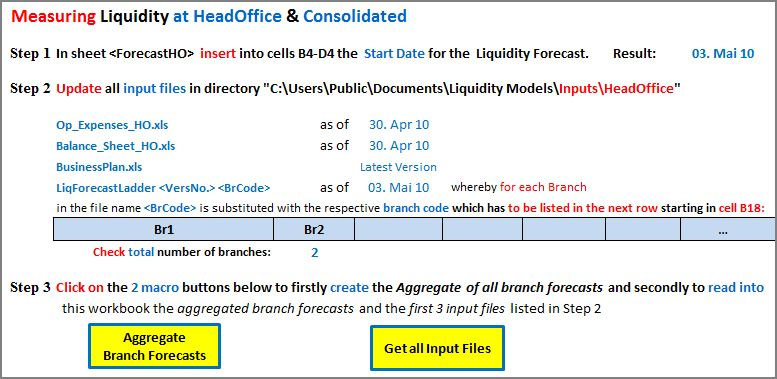

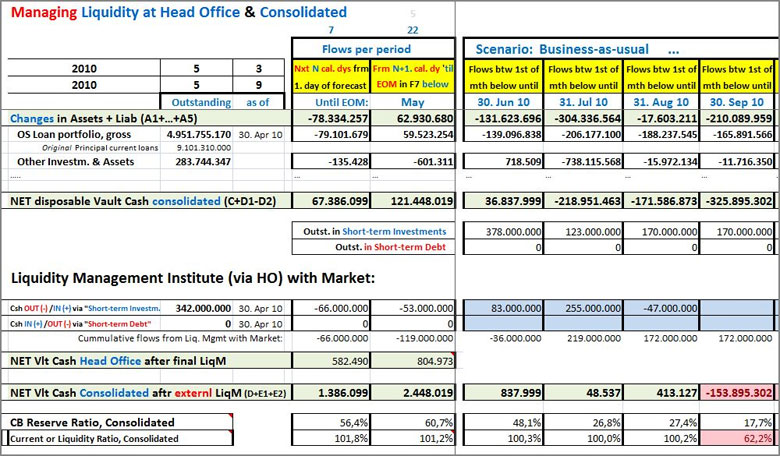

- The Head

Office and Consolidated Liquidity Forecast Ladder covers the above

two periods and additional 11-month period (12 month total)

The cash flows projections are based on the

detailed information such as:

- contractually expected inflows from the debt

service of performing borrowers, adjusted for anticipated arrears

- contractually expected outflows for loan

disbursal and maturing liabilities, with term deposits adjusted for

the “roll over effect”

- experienced level of stability (or “stickiness”) of customer funds with no contractual maturity

- actual / forecasted levels of interest and foreign exchange rates

|

|

Above: Projections of cash flows for the following 11 months are performed with the Consolidated Liquidity Forecast Ladder. These forecasts are based on the resulting numbers for the first two forecast periods and additional parameter settings allowing to incorporate:

- the business plan in a “business-as-usual”

environment

- an adjusted strategy concerning the loan

portfolio, savings & deposits, bank loans, etc. in a liquidity

crisis.

|